In the Buy Here Pay Here (and LHPH) world, payment and affordability are critical components for success. At an average BHPH term of 36 months and APR of 25%, the cost of a vehicle, the markup you can add, and the down payment you collect will ultimately determine the customer’s payment and the likelihood of repayment. You cannot put a credit challenged customer in a $600 per month payment and expect that loan to perform and payments to be made on time.

As used vehicles become more expensive, many BHPH dealers are forced to sacrifice the quality of their inventory in order to keep the overall cost of the vehicle low enough to results in payments their customers can afford. They must buy older vehicles with higher mileage (which bring a greater propensity for mechanical issues), to keep their margins on the initial sale and maintain affordability.

These older, higher mileage vehicles are more likely to have mechanical issues. When a car is not working properly, and customers do not have the money to pay for repairs and the car payment, often these loans will go into default. The result is deterioration in the loan payment performance of these portfolios, directly tied to the risk that there are mechanical problems. This further results in increased service, collections and repossession costs and a negative impact to overall profitability for the BHPH business owner.

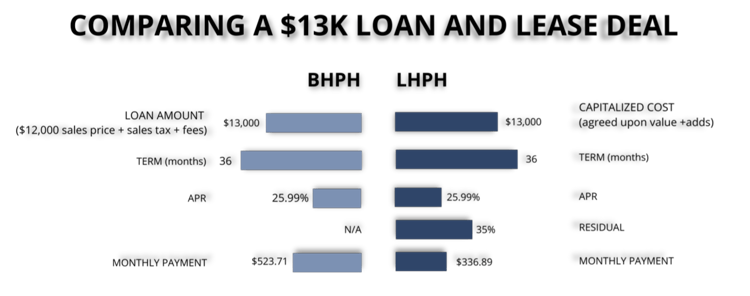

Used car leasing, on the other hand, offers an answer to the challenge of affordability and performance. Thanks to the incorporation of the residual value in the lease, a LHPH dealer can offer a lower monthly payment on the lease of a vehicle with an $13,000 agreed upon value as opposed to a BHPH dealer with the same $13,000 sales price. Both deals provide the consumer the same down payment and the same 36-month term at a 25.99% APR (or IRIL in the lease). However, the LHPH dealer can offer a more affordable payment, likely to last the entire term, and resulting in better portfolio performance over time without sacrificing any profitability to the dealer.

New car prices are likely to remain high, resulting in higher used car costs as well. The Corporate Average Fuel Economy (CAFÉ) standards and new technologies being incorporated into vehicles will contribute to higher prices as well. Therefore, affordability will continue to be a challenge for BHPH dealers, and an opportunity for LHPH dealers, for the foreseeable future.

FEDERAL INCOME TAX DEFERMENT

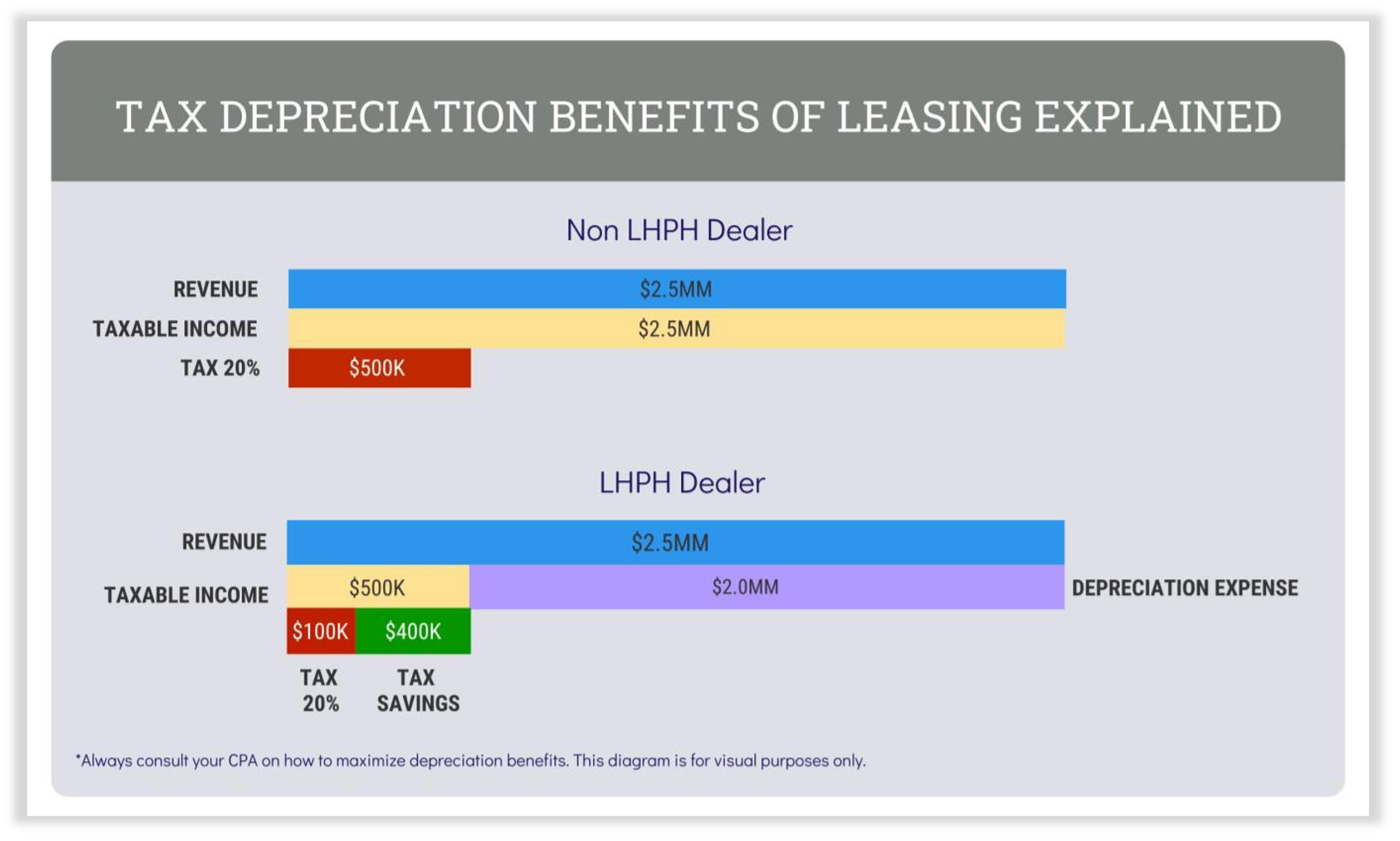

In the used car leasing model, the LHPH dealer becomes the lessor with ownership of the assets they lease to the consumer and retain in their portfolio. This opens new opportunities for the dealership from a tax perspective. The ability to depreciate the assets in your LHPH portfolio over time and report those losses on your Federal Income Tax in the form of a Net Operating Loss (NOL) is another significant advantage of LHPH. These NOL’s can allow a LHPH dealer to reduce their annual income tax liability significantly. While this has always been a compelling reason to migrate to LHPH, the new tax law in 2018 served to compound the benefits of leasing.

Whether you decide to use the bonus depreciation or follow straight-line depreciation standards, either model provides strong advantages over a BHPH portfolio. The 2018 Tax Cut and Jobs Act provided LHPH dealers with the ability to utilize 100% bonus depreciation of used vehicle assets in the first year for leases originated between 2018 and 2023. After that time, the 100% bonus depreciation will decrease by 20% per year. This new law provides another tax savings opportunity for the near future. Alternatively, lessors can follow straight-line depreciation and depreciate the entire value of the asset the first year the vehicle is leased. All up-front profit is deferred, which results in little or no tax liability for the remaining years of the lease.

Either way, there are strong tax advantages to a LHPH program for at least the next four years. It is important to work with your CPA to forecast the impact of bonus and standard depreciation on your current and future tax liability as you assess the right LHPH structure for your business.

SALES TAX ADVANTAGE

With traditional Buy Here Pay Here lending on retail installment sales contracts (RISC), state sales tax is paid at the time of the transaction on the sales price of the vehicle. Typically, this means the dealer uses the entire down payment for sales tax and is immediately cash-negative at the inception of the deal.

For LHPH deals in “pay-as-you-go” states*, the sales tax is calculated only on the actual monies collected by the dealer (i.e. down payment, first payment). Sales tax is then remitted to the state on each lessee payment received for the remainder of the lease. With this structure, the dealer can pay sales tax over time, rather than all up front. This helps dealers start loans on a cash positive basis, requiring less capital to growth the business as well as better unit economics throughout the life of the lease.

For example, if a BHPH dealer sells a car for $15,000 and get a $1,000 down payment on from the customer, in a state with 7% sales tax the dealer would have to pay $1,050 in sales tax to the state before even receiving the first payment from the customer. The entire $1,000 of the customer’s down payment, plus $50 of your own money just went out for tax, and it will take months of successful customer payments before your cash flow recovers from the beginning deficit in cash flow.

If you had leased this vehicle in the same state with “pay-as-you-go” sales tax, you would have paid 7% of the customer’s down payment, or $70 ($1,000 x 7%), in sales tax to the state when you put the vehicle over the curb. The other $930 of that down payment is yours. You are already in a positive cash flow position from the outset. Now the customer will make a $400 per month payment to you, of which you will remit $28 ($400 x 7%) to the state in sales tax each month. Now multiply this impact over the 10, 20, 50 deals you sell per month and leasing quickly makes an incredibly positive impact to your cash flow.

COLLATERAL CONTROL

With a traditional RISC, the dealer or their related finance company is the lien holder on the installment loan. While the lender does have some rights for repossession in the event of a customer default, there are limitations on the process in many states. Right-to-Cure notifications, requirements for Notices of Intent to Sell, and waiting periods that must be offered to the consumer for reinstatement before liquidation of repossessed inventory, among other restrictions. This means additional expenses and delays in the repossession process under a traditional loan.

With a lease, the dealer is the owner of the vehicle (the asset) and named on the title and therefore has many more rights when it comes to the recovery of their property. This can improve recovery times and reduce the post-repossession processes necessary to either lease the vehicle again or wholesale it. As always, you should consult with your local counsel to ensure you are compliant with all state and local laws surrounding consumer repossessions.

BANKRUPTCY REMOTE

Related to collateral control, but worth noting separately when considering the benefits of leasing versus traditional BHPH financing, a lease cannot be included in a bankruptcy. In the event of a bankruptcy filing, the lessee can either assume or reject the lease. If the consumer rejects the lease, they simply return the vehicle to the lessor. If they assume the lease, the lessee continues to make the agreed upon payments for the remaining term. The exposure to the lessor is greatly reduced as there is no redemption for a Chapter 7 or cramdown for a Chapter 13 possible on a lease. This difference results in fewer losses due to bankruptcy in a lease portfolio as compared with a loan portfolio.

CUSTOMER RETENTION

With a traditional BHPH transaction, the dealer makes the sale of the vehicle and will then service the loan through the term. There will be communication throughout the course of the loan, perhaps the customer makes payments at the dealership, or some contact made when a payment is missed. At the end of the contract, or when the customer decides to trade the vehicle, the customer is free to go to any dealership to trade out or they may pay off the vehicle and the vehicle is theirs. If they enjoyed the experience, the dealer may get a repeat customer, but there is no guaranty.

With a LHPH transaction, the dealer maintains significantly stronger customer control. The initial transaction and the collections process are similar. However, considering the value of the asset to the dealer and the desire to turn that asset multiple times, many dealers will roll a warranty into the lease to bring the customer back in for regular maintenance. This maintains the dealer’s asset as well as fosters “customer touch.”

Next, depending on the dealer’s program and lease contract, the customer is made aware they have an option to return the vehicle for a nominal early termination fee. If a quality customer decides they would like to trade up for another vehicle, they can. Many LHPH dealers offer trade up incentives for payment performance allowing a customer to get into a new vehicle before their lease contract comes to term.

For those customers who pay the lease to maturity, the opportunity for retention is far superior to BHPH. The lessee must bring your vehicle back to your dealership when the lease ends. At that time, your sales team can work with them to decide if they would like to purchase the vehicle for the residual value or lease a new vehicle entirely. The opportunity to retain your quality customers with a LHPH product is an incredible advantage over traditional financing.

RESIDUAL CASHFLOW

Not unlike Buy Here Pay Here, the average term on Lease Here Pay Here portfolios tend to hover around 36 months. Therefore, once your dealership has been originating leases for three to four years, your portfolio will begin to mature.

Unlike BHPH, when a LHPH customer completes the term of their lease, they are going to be returning to your dealership to do one of three things:

- The customer may return the vehicle and walk away leaving you with the asset.

- They may choose to return the vehicle and lease another vehicle from you.

- The customer may elect to buy the vehicle from you for the residual value.

Regardless of which decision the customer makes, the dealership will experience an astonishing influx of cash either by wholesaling the vehicle, selling the unit to the customer for the residual, or leasing the paid off vehicle again. Residual cashflow is the most dynamic aspect of leasing and offers incredible opportunities for dealers that remain disciplined in building their portfolios to the maturity inflection point.

FLEXIBILITY TO ADAPT TO CHANGING MARKET CONDITIONS

The landscape in the auto industry is currently experiencing an exciting injection of new, disruptive products and ideas. The future of vehicle technology, consumer affordability relative to vehicle cost, the introduction of ride-share, subscriptions, experimentation with new ownership models, and the ever changing wants and needs of the younger generations has created a degree of uncertainty and opportunity in the industry. The Lease Here Pay Here model provides dealers with the flexibility to adapt to this changing market.

Leasing allows the dealer to overcome the affordability challenges for consumers when compared to the traditional installment loan. A dealer can build their own version of a used-car subscription program by rolling maintenance and insurance into the lessee’s payment. Creative lease programs geared to ride-share drivers are beginning to appear across the country. Even the structure of your leasing program itself can be adjusted over time to adapt to the evolving needs of your local market. LHPH offers dealers a range of opportunities that BHPH simply cannot compete with.

Lease Here Pay Here

Get access to our FREE! e-book and learn how to launch a Lease Here Pay Here program at your dealership. It might just be the best decision you made all year!

Get my FREE! e-book

The roadmap to launching your own LHPH platform requires step-by-step action plan whether you are a current BHPH dealer looking to make the transition or a dealer seeking opportunities to provide lending and transportation solutions to your community while improving your bottom line.

LHPH is the ideal product to bring affordability, profitability, and a competitive advantage to your dealership.